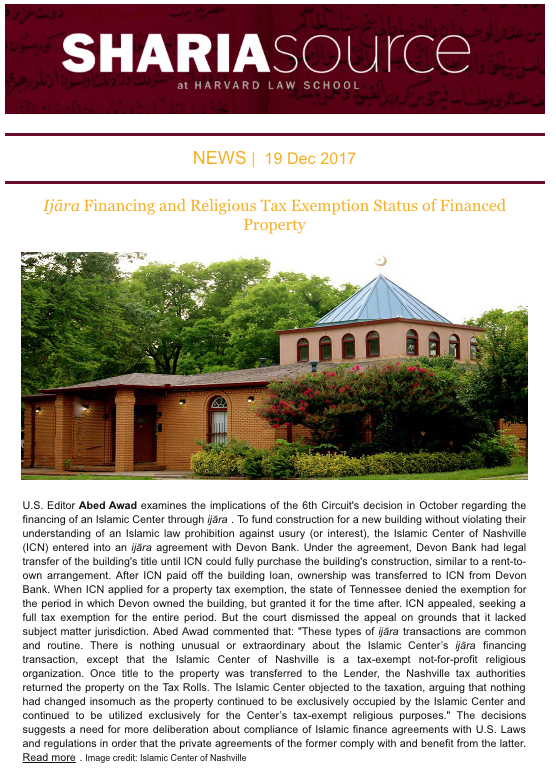

Ijāra Financing and Religious Tax Exemption Status of Financed Property U.S. Editor Abed Awad examines the implications of the 6th Circuit’s decision in October regarding the financing of an Islamic Center through ijāra. To fund construction for a new building without violating their understanding of an Islamic law prohibition against usury (or interest), the Islamic Center of Nashville (ICN) entered into an ijāra agreement with Devon Bank. Under the agreement, Devon Bank had legal transfer of the building’s title until ICN could fully purchase the building’s construction, similar to a rent-to-own arrangement. After ICN paid off the building loan, ownership was transferred to ICN from Devon Bank. When ICN applied for a property tax exemption, the state of Tennessee denied the exemption for the period in which Devon owned the building, but granted it for the time after. ICN appealed, seeking a full tax exemption for the entire period. But the court dismissed the appeal on grounds that it lacked subject matter jurisdiction. Abed Awad commented that: “These types of ijāra transactions are common and routine. There is nothing unusual or extraordinary about the Islamic Center’s ijāra financing transaction, except that the Islamic Center of Nashville is a tax-exempt not-for-profit religious organization. Once title to the property was transferred to the Lender, the Nashville tax authorities returned the property on the Tax Rolls. The Islamic Center objected to the taxation, arguing that nothing had changed insomuch as the property continued to be exclusively occupied by the Islamic Center and continued to be utilized exclusively for the Center’s tax-exempt religious purposes.” The decisions suggests a need for more deliberation about compliance of Islamic finance agreements with U.S. Laws and regulations in order that the private agreements of the former comply with and benefit from the latter. Read more. Image credit: Islamic Center of Nashville

Ijāra Financing and Religious Tax Exemption Status of Financed Property U.S. Editor Abed Awad examines the implications of the 6th Circuit’s decision in October regarding the financing of an Islamic Center through ijāra. To fund construction for a new building without violating their understanding of an Islamic law prohibition against usury (or interest), the Islamic Center of Nashville (ICN) entered into an ijāra agreement with Devon Bank. Under the agreement, Devon Bank had legal transfer of the building’s title until ICN could fully purchase the building’s construction, similar to a rent-to-own arrangement. After ICN paid off the building loan, ownership was transferred to ICN from Devon Bank. When ICN applied for a property tax exemption, the state of Tennessee denied the exemption for the period in which Devon owned the building, but granted it for the time after. ICN appealed, seeking a full tax exemption for the entire period. But the court dismissed the appeal on grounds that it lacked subject matter jurisdiction. Abed Awad commented that: “These types of ijāra transactions are common and routine. There is nothing unusual or extraordinary about the Islamic Center’s ijāra financing transaction, except that the Islamic Center of Nashville is a tax-exempt not-for-profit religious organization. Once title to the property was transferred to the Lender, the Nashville tax authorities returned the property on the Tax Rolls. The Islamic Center objected to the taxation, arguing that nothing had changed insomuch as the property continued to be exclusively occupied by the Islamic Center and continued to be utilized exclusively for the Center’s tax-exempt religious purposes.” The decisions suggests a need for more deliberation about compliance of Islamic finance agreements with U.S. Laws and regulations in order that the private agreements of the former comply with and benefit from the latter. Read more. Image credit: Islamic Center of Nashville

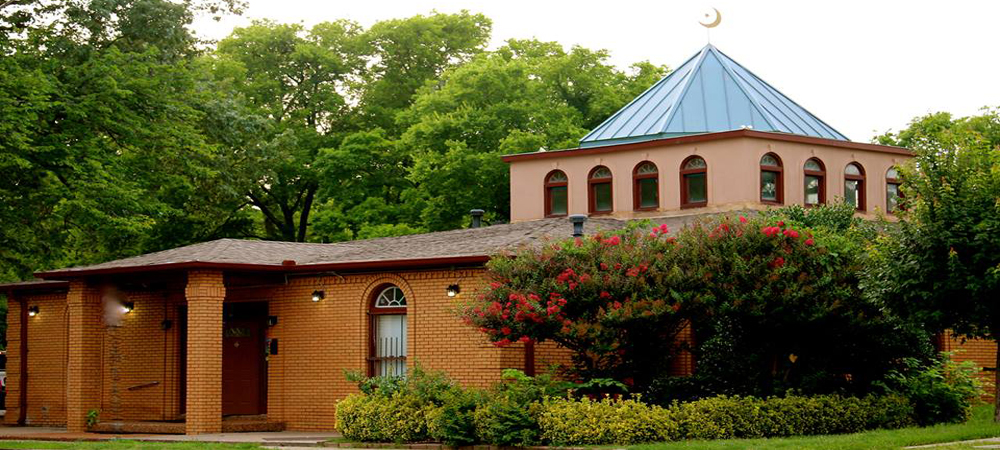

Islamic Center of Nashville v. Tennessee ( M.D. Tenn 2016 & 6th Cir. 2017 ): Tax Status of I jāra -Financed Center When the Islamic Center of Nashville sought to finance its center without paying interest, it entered into an agreement with a local bank that might have complied with Islamic law but been at odds with current understandings of tax exempt law. The state of Tennessee denied the Center’s request for tax exemption for the time period in which the local bank owned the building. ICN appealed the decision, but the trial court found that it had no subject matter jurisdiction to hear the case. The U.S. Court of Appeals for the Sixth Circuit affirmed the district court’s decision. Read more. Image credit: Wikipedia

Islamic Center of Nashville v. Tennessee ( M.D. Tenn 2016 & 6th Cir. 2017 ): Tax Status of I jāra -Financed Center When the Islamic Center of Nashville sought to finance its center without paying interest, it entered into an agreement with a local bank that might have complied with Islamic law but been at odds with current understandings of tax exempt law. The state of Tennessee denied the Center’s request for tax exemption for the time period in which the local bank owned the building. ICN appealed the decision, but the trial court found that it had no subject matter jurisdiction to hear the case. The U.S. Court of Appeals for the Sixth Circuit affirmed the district court’s decision. Read more. Image credit: Wikipedia

Muslim Cmty. Ass’n of Ann Arbor & Vicinity v. Pittsfield Charter Twp. (E.D. Mich. 2013): Discrimination in Zoning Regulations The Plaintiff, the Muslim Community Association of Ann Arbor, challenged the Pittsfield Charter Township for its refusal to re-zone the area surrounding the Plaintiff so that the Plaintiff could expand and build a school. Although an independent outside planner endorsed the rezoning, the Plaintiff alleged that the Respondents denied rezoning due to concerns stemming largely from an animus to the Islamic faith. The Plaintiff claimed that the Respondents discriminated against the organization in violation of the Religious Land Use and Institutionalized Persons Act, the Fourteenth and Fifth Amendments of the U.S. Constitution, and “state law claims” in the Michigan state constitution. Read more. Image credit: Wikipedia

Muslim Cmty. Ass’n of Ann Arbor & Vicinity v. Pittsfield Charter Twp. (E.D. Mich. 2013): Discrimination in Zoning Regulations The Plaintiff, the Muslim Community Association of Ann Arbor, challenged the Pittsfield Charter Township for its refusal to re-zone the area surrounding the Plaintiff so that the Plaintiff could expand and build a school. Although an independent outside planner endorsed the rezoning, the Plaintiff alleged that the Respondents denied rezoning due to concerns stemming largely from an animus to the Islamic faith. The Plaintiff claimed that the Respondents discriminated against the organization in violation of the Religious Land Use and Institutionalized Persons Act, the Fourteenth and Fifth Amendments of the U.S. Constitution, and “state law claims” in the Michigan state constitution. Read more. Image credit: Wikipedia

See the full newsletter.